3 ideas to beat income tax bracket creep

Income tax “bracket creep” happens when an increase in income moves you from one tax bracket to the next, resulting in a higher tax rate, and therefore reducing the overall gain from your higher salary.

In it’s tax discussion paper the Government defines bracket creep as referring “to the fact that taxpayers will face higher average, and sometimes marginal, tax rates over time even if their income has only increased by inflation”. So, bracket creep can occur simply because income tax brackets are not increased to account for inflation. However, bracket creep can also happen, for example, from a pay rise that pushes the taxpayer into a higher bracket.

The Australian government has said it is looking for ways to combat bracket creep – like making smaller brackets or adjusting them for inflation – but in the meantime, here’s how you can reduce the impact if bracket creep is threatening you.

First let’s look at how bracket creep affects the average working taxpayer in Australia.

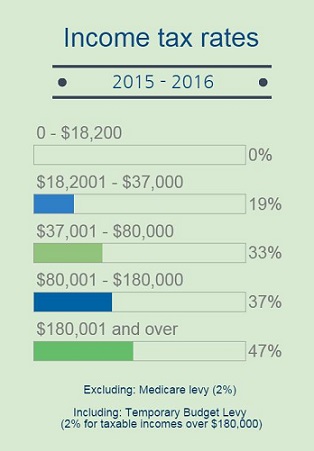

Jackie earned $179,000 a year (excluding super) during 2014-15. She sat in the $80,001 to $180,000 tax bracket, so her income in that bracket was taxed at 37%*. Her employer offered her a raise of $11,000 a year. Jackie was thrilled to earn $190,000, but she unknowingly crept into the next tax bracket.

The tax rate for her new bracket (more than $180,000) is 47%*. As she enters the higher bracket, her additional tax payable, because of the $11,000 pay rise, is $5,070 a year. Were Jackie left within her previous bracket, her pay rise would have attracted $4,070 in extra tax — in other words, she is now liable to an additional $1,000 in tax.

(*Excluding the Medicare levy but including Temporary Budget Repair Levy, if applicable.)

What options are there for Jackie, and other Australian taxpayers, to lessen this burden?

Option 1. Salary sacrifice the additional income

Instead of accepting the higher salary as purely taxable income, Jackie decides to sacrifice an extra $10,000 into her super. That way, her taxable income is reduced to keep her in the lower tax bracket, and that $10,000 yearly super injection ends up being taxed at only 15% (although she will need to consider contribution caps).

Super isn’t the only avenue. Consider speaking to your employer about a novated leasing arrangement. Salary packaging a car is another a good way to potentially reduce your taxable income if you need a nice new set of wheels.

Option 2. Negatively gear properties and/or shares

Many shrewd taxpayers out there are quick to tout the benefits of negative gearing. While you shouldn’t misconstrue the day-to-day arrangements as anything but an economic loss, offsetting that loss against your taxable income may be a good way to reduce your taxable income and stay in a lower tax bracket.

Option 3. Push back your deductions

If you’re on the verge of creeping into the next tax bracket and you think it’ll happen in the next financial year, consider paying any deductible expenses after June 30. Membership fees, course fees, technical resource expenses and so forth may prove more advantageous if deducted later rather than sooner.